To understand whether inflation acts as a tax, the causes and underlying mechanics of inflation must be understood. Inflation, or the rise in prices, is a decline in purchasing power of your income and savings. In free markets, inflation occurs naturally when demand outstrips supply. Loosened monetary and fiscal policies drove the inflationary environment over the last few years. More specifically, inflation was caused by the Federal Reserve increasing the amount of money printed by the US Treasury Department. The federal government’s deficit spending, energy and other policies caused a supply-demand imbalance and thus exacerbated inflation.

Mechanically, inflation benefits borrowers at the expense of creditors. A simple loan of $10,000 at 5% due in one year from now would result in the borrower owing the creditor $10,500 in one year’s time. But if inflation is 10% during that year, the amount the borrower owes is still $10,500 – there is no appreciation in the amount due. In hindsight the inflation premium factored into the 5% rate was too low to recover the loss in purchasing power. Since the federal government is a massive borrower via deficit spending, like taxes, the federal government gains during periods of high inflation at the expense of Americans and Treasury Bond investors. Therefore, inflation redistributes your wealth to the federal government similar to the income taxes that the federal government collects from you.

The Inflation Tax is the amount of wealth that is transferred from households and businesses to the federal government as a result of inflation.[1]

The federal government taxes individuals and businesses based on a percentage of their income or net income generated during a fiscal year. Although federal income tax rates may change from year to year, the federal government only collects income taxes from income-producing citizens and businesses. On the other hand, inflation affects your total wealth, not just the income earned during that year. The severity or harm of inflation depends not only on your financial condition but also on both the inflation rate and on the duration of the inflationary environment.

Examining whether inflation or taxes hurt you more during the last three years is best illustrated by following example. Assuming the normal inflation rate is 2%, we can calculate how much higher the federal income tax rate would have to be to compensate for the loss in purchasing power and destruction of wealth resulting from high inflation.[2]

Let us suppose you had the following financial position at the start of July 1st, 2020:

- Annual Salary: $200,000

- Expected Salary Annual Growth Rate: 9%[3]

- Effective Tax Rate: 30%

- After-tax Savings Rate: 20%

- Beginning Savings / Investment Portfolio: $0

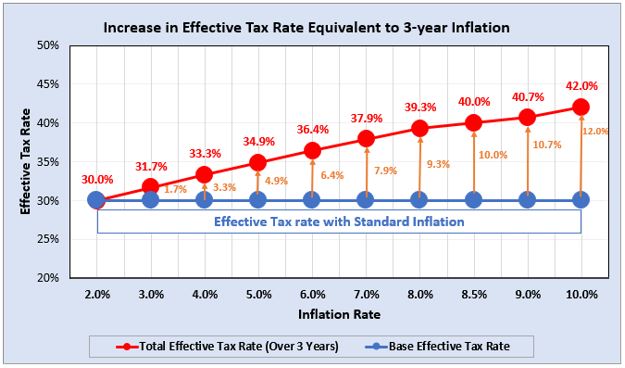

As displayed in the chart and table below, the cost imposed by the last three years’ annual average inflation of 6.0% was equivalent to paying an additional federal income tax rate of 6.4% for each of those years. The results regarding the aforementioned financial position are displayed in the chart below, which shows the equivalent federal income tax rates assuming varying levels of inflation over a 3-year period.

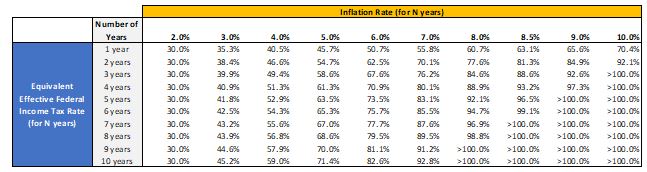

The table below indicates the equivalent effective federal income tax rates, assuming varying levels of inflation lasting from one to ten years. As displayed in the table, the equivalent effective federal income tax rate goes up markedly as the inflation rate increases, and the longer the inflation rate is sustained. Higher inflation rates have a devastating impact on your savings and its real value will diminish significantly in persistent inflationary environments. For instance, the 30% federal income tax rate is equivalent to a 65.8% federal income tax rate for each year if 10% per year inflation lasts for 10 years.

Effective Tax Rate Equivalent to Varying Intensities and Durations of Inflation (Zero Beginning Savings or Investment)

Further, the cost of inflation is substantially worse if you also have a savings or investment account. If you have a savings or investment portfolio of $1,000,000 and the inflation rate is 10.0%, your loss in purchasing power would be $100,000 in a single year. Of course, your $1,000,000 investment portfolio would (and hopefully) appreciate during the year, which would make up for a portion of this loss in purchasing power. Assuming that there are no reinvestment gains or losses for simplicity, this $100,000 loss would be equivalent to an additional 50% income tax on a $200,000 salary.

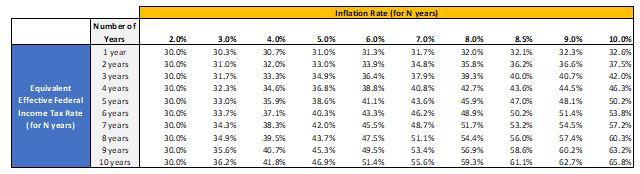

Now suppose you are in the same financial position as before with the addition of having a $400,000 investment portfolio to begin with. Due to your investment portfolio’s substantial decline in worth caused by inflation, the cost imposed by the last three year’s annual average inflation of 6.0% was equivalent to paying additional federal income taxes at a rate of 67.6% for each of those years. This is 37.6% more than the 30.0% effective tax rate. A federal income tax rate greater than 100.0%, a non-sensical but real tax, would be the Inflation Tax if inflation were to remain at 10% for 10 years.[4] In large part this is due to the wealth destruction of your investment portfolio.[5]

The table below indicates the equivalent effective federal income tax rates, assuming varying levels of inflation lasting from one to ten years, assuming you have the $400,000 investment account to begin with.

Effective Tax Rate Equivalent to Varying Intensities and Durations of Inflation ($400,000 Beginning Savings / Investment Amount)

The inclusion of an investment account results in equivalent federal income tax rates that are much higher. The greater the value of your investment account the higher the equivalent federal income tax rates, as indicated by the relative differences between the tables with and without the investment portfolios. Therefore, the intensity of the Inflation Tax is larger when you have greater wealth.

So, are increases to the federal income tax rate or the Inflation Tax ultimately worse for you? The answer depends on your financial position and how well you invest to offset the effects of inflation.[6] But in most cases you would be much better off with a rise in the federal income tax rate than the Inflation Tax.[7]

The next time a politician mentions that 10% inflation is like being taxed an additional 10%, the truth is far worse. The Inflation Tax affects your entire wealth, no matter how much or little income you are receiving.

The value of your specific business may also be positively or negatively affected by periods of high inflation. Any changes in value resulting from high inflation are dependent on numerous factors including your ability to successfully transfer price hikes for your products or services to customers, your increased costs for materials, equipment, energy, rent, and labor, as well as any changes to your business’ perceived risk and cost of capital.